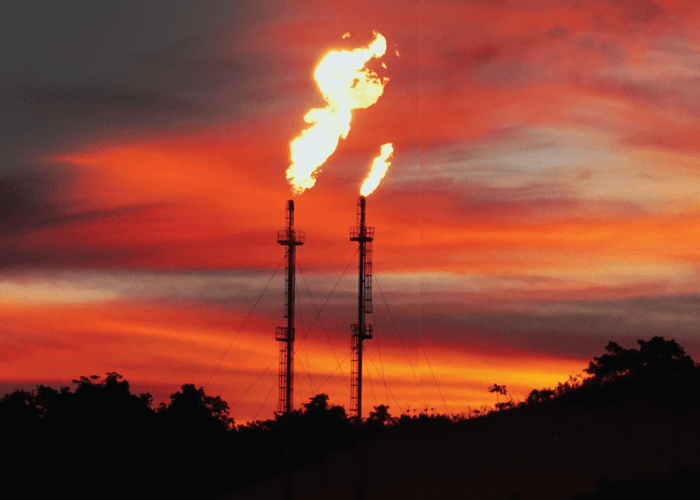

WHAT IS FLARING?

Gas flaring is the combustion of natural gas as waste. While flaring occurs in a number of industrial processes including petrochemical production and landfill operation, in this proposal we focus on the largest source of flaring: oil production, for which the combustion of associated gas represents the majority of flared gas volumes. Natural gas is often produced as a by-product during oil extraction where it is known as associated gas.

Despite being a valuable resource in its own right, natural gas can be flared for numerous reasons:

Lack of gas capture and transportation infrastructure. Companies may produce oil without the infrastructure to transport away the associated gas. This might occur when the amount of associated gas is small, when there is a lack of a viable market for the captured gas, or where the operator has initiated oil production in advance of completing the necessary gas infrastructure.

Lack of on-site uses. Associated gas can be utilized in several ways such as re-injection into the hydrocarbon-bearing geology to provide pressure support, or conversion to compressed natural gas (CNG) or liquefied natural gas (LNG) for offtake by truck or other modalities. When none of those are in place, the gas must be flared.

Midstream bottlenecks. In some cases, gas transportation infrastructure may be in place, but capacity constraints, maintenance or other factors may prevent the offtake of the gas. This is more likely when the gas network is not under the control of the oil producer.

Safety. A build-up of pressure, which may result from an increase in gas flow as well as downstream bottlenecks may require flaring. Equipment malfunctions that shut down sections of the gas handling process may also cause situations where safety-related flaring is required.

If a producer cannot transport gas away for any of these reasons, the gas must be flared, given that flaring is preferable to venting natural gas directly into the atmosphere.

Most flaring can be classified as being either routine or event-driven, reflecting the reasons that the flaring is taking place.

Routine flaring. This occurs when gas is flared due to a lack of infrastructure to offtake the gas or use it onsite. In some cases, oil production is started before necessary infrastructure to transport the associated gas is put in place. If this takes place in less than a year, the flaring is considered temporary routine flaring; otherwise it is called long-term routine flaring.

By contrast, event-driven flaring is episodic in nature and occurs when operators flare for safety or maintenance. This can be caused by infrastructure events such as outages and accidents, and midstream takeaway constraints, primarily insufficient pipeline capacity.

THE PROBLEM

Natural gas flares emit carbon dioxide, smog-forming nitrogen oxides, and other pollutants that are damaging to human health. When natural gas is released without burning, for example due to a flare malfunction, large quantities of climate-warming methane can be released directly into the atmosphere. Flaring and venting are highly visible evidence of pollution and waste by oil and gas operators. In the words of one executive, flaring is a “black eye” for the industry.

PATHWAY FRON FLARE TO CARBON CREDITS

1

Screen & quantify using satellite data (FlareIntel, World Bank tracker) to rank flares by volume & economics.

2

Feasibility & baseline studies per AM0009/AM0037: 3-year historic flare log, regulatory analysis.

3

Technology selection (FGRU, reinjection, gas-to-power, mini-LNG).

4

Draft PDD → public comment on Verra Hub (30 days).

5

Validation audit (VVB) + stakeholder consultation (communities & regulators).

6

Financial close: credits often forward-sold to offtakers (e.g., Shell Decarbonisation Desk) at US $6–12 / tCO₂e.

7

Construction & commissioning; baseline metering continues for first monitoring period.

8

Verification & VCU issuance every 1–2 yrs; sale via broker or direct to buyer.

Timeline: 18–24 months for first credits if permits and gas offtake contracts are in place; longer if greenfield pipelines required.

MARKET OUTLOOK

- Credit supply is tiny: <5 Mt CO₂e yr-¹ of flare-gas VCUs were issued globally in 2024; demand from buyers looking for industrial-sector credits (>100 Mt in 2025) dwarfs supply.

- Regulatory drivers: Nigeria’s rising penalties and Angola’s LNG expansion spur capture economics even without credits—projects must prove that flare capture would not occur anyway (additionality).

- White-space niches: ○ Marginal, stranded onshore flares (<3 MMscf d-¹) where credits tip payback < 3 yrs.

- Integrated flare-gas-to-power for modular data centres (AI/bitcoin) with dual revenue.

- High-resolution MRV tech (satellite + on-site IoT) needed for robust Verra validation.

Bottom line: The sector is far from saturated—but only robust, additional projects with transparent monitoring will win both regulatory approval and premium credit buyers.